The most closely watched press conference in American finance this year happens today. The Kevin Warsh first Fed meeting as Chair of the Federal Reserve concludes this afternoon, with an interest rate announcement at 2:00 PM Eastern Time followed by his debut press conference at 2:30 PM. As StockTitan’s live preview of the meeting explained, the actual rate decision is almost a foregone conclusion, with futures markets pricing in roughly a 97 percent probability that rates stay unchanged. The real story is everything happening around that number, from the first policy signals of an entirely new era at the central bank to a direct, public conflict between the new Fed Chair and the president who appointed him.

Who Is Kevin Warsh and How Did He Get Here

Kevin Warsh was sworn in as the 17th Chair of the Federal Reserve on May 22, 2026, succeeding Jerome Powell. As FXStreet’s analysis of the transition detailed, Warsh was confirmed by the Senate in a 54-45 vote, with the swearing-in ceremony taking place at the White House and Supreme Court Justice Clarence Thomas administering the oath. His nomination was first announced back in February 2026, a moment that one financial commentary described as sending shockwaves through global fixed-income markets at the time.

Warsh is not a newcomer to the Fed. He previously served as a Federal Reserve Governor from 2006 to 2011, giving him direct experience inside the institution during the 2008 financial crisis. What sets his return apart is the mandate he has signalled for his second act: a more disciplined, less interventionist Fed that talks less and moves with more conviction once it does act.

A Self-Described Reformer

At his swearing-in ceremony, Warsh pledged what he called a reform-oriented Federal Reserve focused on integrity and policy discipline. According to FXStreet’s reporting on his confirmation hearing comments, Warsh told senators he favoured what he called messier meetings where policymakers could have a good family fight, signalling a clear preference for more open internal debate before the committee settles on a final decision, a departure from the carefully managed consensus-building approach that has characterised the Fed in recent years.

What Is Actually Being Decided Today

Today’s meeting is the conclusion of a two-day FOMC gathering that began June 16. It is also a quarterly projection meeting, meaning it produces more than just a rate decision. The committee will release an updated Summary of Economic Projections, including a fresh dot plot showing where individual Fed officials expect interest rates to land over the coming years.

The Rate Decision Itself

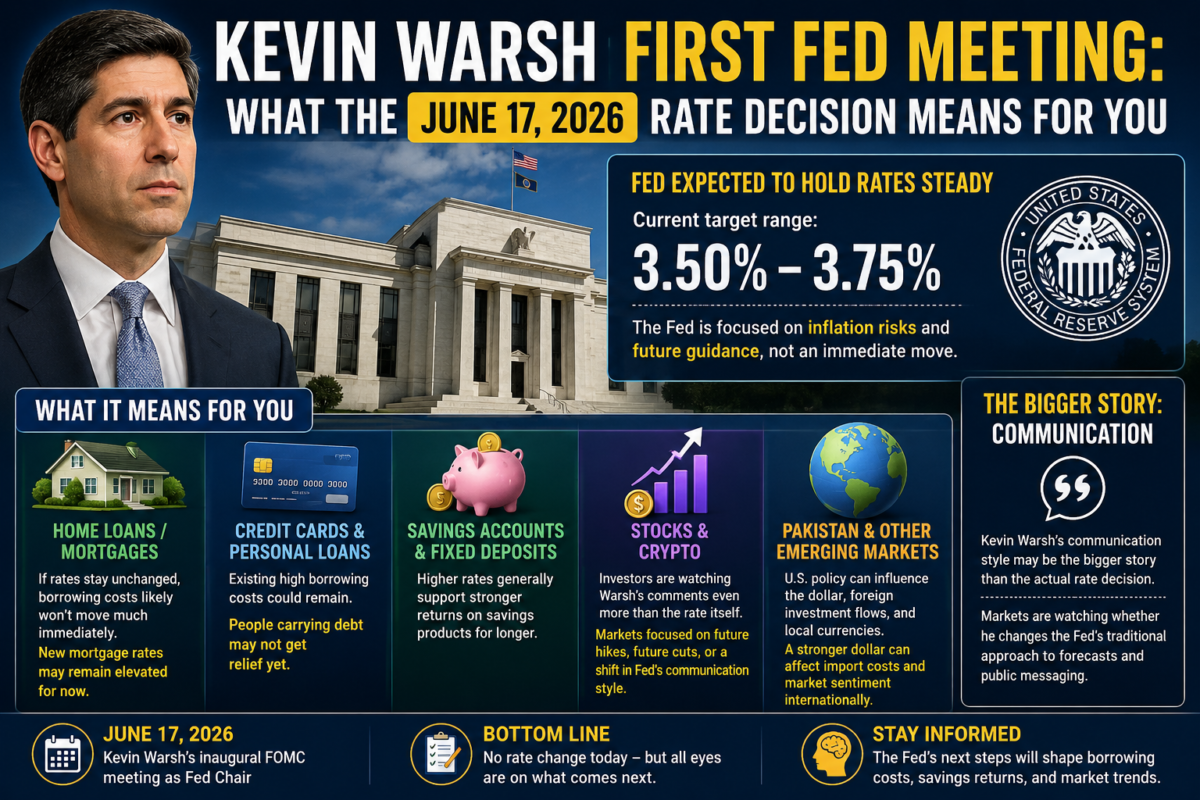

The Federal Reserve has held its benchmark federal funds rate steady in a range of 3.50 percent to 3.75 percent across several consecutive meetings since December 2025. As StockTitan reported, CME FedWatch futures pricing put the odds of another hold at roughly 97 percent as of June 13, 2026, and a Reuters poll of 102 economists found 72 of them expecting no change in rates through the remainder of 2026.

The More Important Detail: The Easing Bias

Beyond the headline rate, the specific language in the Fed’s policy statement is being watched extremely closely. As Chase’s investor-focused preview of the meeting noted, the Fed is not expected to move rates in June and is likely to remain on hold for the rest of 2026, but there will likely be an explicit move away from a bias toward easing to a neutral stance on rates.

This shift matters more than it might sound. The Fed’s previous statements contained language signalling an inclination toward future rate cuts, often referred to as an easing bias. Removing that language would be a clear signal to markets that further rate cuts are not on the immediate horizon, even though the headline rate itself is not moving today. For anyone with a mortgage, a savings account, or a business loan tied to floating rates, this distinction between the rate itself and the language describing future intentions is exactly the kind of detail that moves markets in the hours after the announcement.

Why Inflation and the Iran War Both Matter to This Decision

Two major economic forces are shaping this meeting’s backdrop. As detailed in coverage of the meeting, inflation is currently hovering at a three-year high of 3.8 to 4.2 percent, well above the Fed’s 2 percent target. That alone would argue against any near-term rate cuts, since lowering borrowing costs while inflation runs hot risks fuelling further price increases.

At the same time, the newly announced agreement between the United States and Iran to end their war and reopen the Strait of Hormuz has triggered a meaningful drop in energy prices in recent days, according to the same reporting. Lower energy costs take some of the immediate pressure off inflation, giving the Fed a bit more room to manoeuvre than it would have had if the Middle East conflict and its associated energy price spike had continued unresolved.

Adding further complexity, the labour market has been running stronger than expected. According to analysis of the meeting’s backdrop, the US economy added 172,000 jobs in a recent report, far above expectations, a figure strong enough that Goldman Sachs reportedly dropped its forecast for a December 2026 rate cut entirely, pushing its expected timeline for the next cut into 2027.

The Political Pressure Campaign Warsh Is Walking Into

What makes this particular Fed meeting genuinely unusual is the open political pressure surrounding it. President Trump specifically selected Warsh because he wanted lower interest rates, having repeatedly criticised Jerome Powell for not cutting rates fast enough during his tenure. As one detailed analysis of the situation put it, Trump even said in February 2026 that he would not have chosen Warsh if Warsh wanted rate hikes.

But the economic data has moved in the opposite direction from what that appointment anticipated. Inflation rose rather than fell. The jobs market strengthened rather than weakened. Both of these developments make the case for rate cuts considerably weaker than it appeared earlier in the year. Trump nonetheless went public again just before this meeting, stating there was no reason to raise rates and that the Fed should be lowering them, a comment made directly in the days leading up to Warsh’s first major decision as Chair.

This creates a genuinely difficult position for Warsh in his very first meeting. As Quartz’s coverage of the dynamic described it, Warsh is heading into his first FOMC meeting facing pressure from two directions, a bond market betting that interest rates may need to rise and a president insisting they should fall. JPMorgan’s chief economist Michael Feroli told CNBC that an explicit embrace of rate hikes from Warsh seems unlikely in this first meeting, though he noted Warsh might leave the door open by saying he cannot rule it out entirely.

Since taking office, Warsh has offered virtually no public comment on interest rate policy, a deliberate silence that has left investors with very little to work with heading into today’s announcement. That makes his press conference at 2:30 PM Eastern arguably more consequential than the rate decision itself, since it will be the first real window into how he balances institutional independence against the political reality of the president who appointed him.

A New Communication Style at the Fed

Beyond the substance of monetary policy, Warsh has signalled significant changes to how the Fed communicates with the public and with markets. According to reporting on his approach, Warsh has criticised the Fed’s historical reliance on continuous public forecasting and has hinted at a regime change, intending to introduce a scaled-back, less-is-more communication approach.

This represents a meaningful philosophical shift from the Fed’s recent practice of heavily pre-signalling its future moves through detailed forward guidance, speeches, and frequent commentary from individual Fed officials. A less-is-more approach could mean fewer hints about future rate moves, which would make Fed policy somewhat less predictable in the near term but could also reduce the kind of market overreaction to every individual comment from Fed officials that has characterised recent years.

What This Means for Your Money

Mortgages and Home Loans

With rates holding steady at 3.50 to 3.75 percent and most economists not expecting cuts for the remainder of 2026, anyone hoping for a near-term drop in mortgage rates should not expect significant relief in the coming months. Mortgage rates are influenced by the Fed’s policy rate but also by longer-term Treasury yields and broader market expectations, both of which have already priced in a steady-rate environment for now.

Savings Accounts and CDs

The flip side of steady rates is that savers benefiting from higher-yield savings accounts and certificates of deposit are likely to continue enjoying those returns for a while longer. If the Fed does eventually signal cuts later in 2026 or into 2027, locking in current CD rates now could be a reasonable strategy for anyone trying to maximise returns on cash savings before rates potentially decline.

Credit Cards and Variable-Rate Debt

Interest rates on credit cards and other variable-rate debt products are likely to remain at current elevated levels with rates holding steady. Anyone carrying significant credit card debt should not expect meaningful relief from Fed policy in the near term and may want to prioritise paying down high-interest debt rather than waiting for borrowing costs to fall.

The Stock Market

Markets generally prefer predictability, and Warsh’s press conference today will be parsed intensely for any signals that diverge from what is currently priced in. If Warsh’s tone comes across as notably more hawkish, more concerned about inflation, than markets currently expect, stocks could react negatively in the short term. If his comments are interpreted as more dovish or open to future cuts than expected, the opposite reaction is possible. The energy price relief from the US-Iran agreement reached this week adds another layer of complexity markets will be weighing alongside the Fed’s own signals.

What Happens Next

Today’s meeting is widely seen as a transitional one, more about establishing Warsh’s communication style and institutional approach than about making a dramatic policy move. The real tests of his leadership will likely come at subsequent meetings later in 2026, particularly if inflation data or labour market figures shift meaningfully in either direction, forcing the committee toward an actual change in the federal funds rate rather than another hold.

Investors, businesses, and everyday Americans managing mortgages, savings, and debt will all be watching the same fundamental question over the coming months: does Kevin Warsh’s Federal Reserve ultimately bend toward the lower rates the president has been pushing for, or does it hold an independent line dictated by the inflation and employment data in front of it. Today’s meeting offers the first real clues, even if the headline rate itself does not move.

Frequently Asked Questions (FAQs)

Q1. Did the Federal Reserve change interest rates on June 17 2026?

No. The Federal Reserve held its benchmark federal funds rate steady in the range of 3.50 percent to 3.75 percent, in line with market expectations. CME FedWatch futures had priced in roughly a 97 percent probability of a hold heading into the meeting, and the rate decision itself was widely seen as a foregone conclusion.

Q2. Who is Kevin Warsh and when did he become Fed Chair?

Kevin Warsh is the 17th Chair of the Federal Reserve, sworn into office on May 22, 2026, succeeding Jerome Powell. He was confirmed by the Senate in a 54-45 vote and previously served as a Federal Reserve Governor from 2006 to 2011. The June 16-17, 2026 meeting was his first as Chair.

Q3. Why does Trump want Kevin Warsh to cut interest rates?

President Trump nominated Warsh specifically because he wanted a Fed Chair who would pursue lower interest rates, having repeatedly criticised former Chair Jerome Powell for not cutting rates fast enough. However, rising inflation and a stronger than expected labour market have made the case for near-term rate cuts considerably weaker since Warsh’s nomination.

Q4. What is the easing bias and why does removing it matter?

The easing bias refers to language in the Fed’s policy statement that signals an inclination toward future interest rate cuts. Economists widely expect Warsh’s Fed to drop this language in favour of a neutral stance, which would signal to markets that further rate cuts are not imminent, even though the headline interest rate itself is not changing in this particular meeting.

Q5. How will this Fed decision affect mortgage rates?

With the federal funds rate holding steady and most economists not expecting cuts through the remainder of 2026, mortgage rates are unlikely to see significant near-term relief. Mortgage rates are influenced by the Fed’s policy rate as well as broader Treasury yield movements, both of which have already priced in a steady-rate environment.

Q6. What is Kevin Warsh’s approach to Fed communication going forward?

Warsh has signalled a significant shift away from the Fed’s recent practice of heavily pre-signalling future policy moves through extensive public commentary. He has described a preference for a scaled-back, less-is-more communication approach and has said he favours more open internal debate among policymakers before the committee reaches a final decision.

The Kevin Warsh first Fed meeting marks the beginning of a genuinely new chapter for the institution that sets the cost of money for the entire American economy. While today’s rate decision itself changed little, the underlying signals, the language shifts, the dot plot, and the tone of his first press conference, will shape how investors, businesses, and everyday Americans think about borrowing costs for the rest of 2026 and beyond. With political pressure pulling in one direction and economic data pulling in another, Warsh’s ability to navigate that tension starting today will define the early character of his tenure. For more business and finance news as this story develops, keep reading Weblogs4u.